TL;DR:

- Most Ontario bank transactions only require presenting original government-issued ID, not notarized documents. Notarization becomes necessary for higher-stakes legal or financial matters such as mortgage affidavits, powers of attorney, or estate documents to verify authenticity. Proper preparation and early coordination with lenders and notaries help ensure smooth processing and avoid delays.

Many Ontarians walk into their bank expecting to hand over a stack of notarized paperwork, only to find out the teller just wants to see their driver’s license. On the other hand, some borrowers show up to a mortgage closing without a single notarized document and quickly discover the deal cannot move forward. Opening a bank account in Ontario typically requires government-issued ID, not notarized copies of your ID. Knowing exactly when notarization is required, and when it is not, saves you time, money, and a lot of frustration.

Table of Contents

- When do banks require notarized documents?

- Essential documents banks may ask you to notarize

- How to get documents notarized for banks in Ontario

- Key mistakes and expert tips for notarization success

- The practical truth about notarized bank documents in Ontario

- Get help with notarized banking documents in Ontario

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Notarization is situational | Banks only require notarized documents for specific cases like loans, not for regular account opening. |

| Know what documents need | Check with your bank for an official document checklist before starting the process. |

| Plan for timelines | Delays often result from late requests or outdated paperwork; clarify validity window requirements. |

| Online options speed things up | Online notarization can cut processing times—make sure your bank accepts digital notarization. |

| International use brings extra steps | Authentication or an apostille may be needed for documents used outside Canada. |

When do banks require notarized documents?

The confusion here is completely understandable. The word “notarized” gets thrown around loosely in banking conversations, and many people assume it applies to every document they bring to a financial institution. That is rarely true.

For standard everyday banking, such as opening a personal checking or savings account, Ontario banks want to see original government-issued ID in person. A notarized copy of your passport will not substitute for showing the actual passport. These are two separate things, and conflating them causes real problems.

Notarized documents become relevant when the stakes are higher, when there is a legal relationship, significant money, or institutional trust that needs to be formally established. The online notarization process is most commonly triggered in these banking situations:

- Mortgage and loan applications that require sworn affidavits confirming financial standing or property use

- Powers of attorney allowing someone to act on behalf of an account holder

- Business account setup requiring corporate resolutions or letters of authority

- International or foreign account documentation where the receiving institution cannot verify identities in person

- Estate and probate banking matters where an executor needs legal authority to access funds

- Beneficiary designation changes on registered accounts or insurance products held through a bank

Understanding notary public ID requirements is a smart first step before you book any notarization appointment. Showing up with the wrong ID wastes everyone’s time.

Key distinction: Notarization is not a replacement for presenting original identification at a bank. It is a separate legal step that confirms the authenticity of a specific document or signature for a specific purpose.

Essential documents banks may ask you to notarize

Now that you know when notarized documents are required, let us look at which documents banks are most likely to request with notarization. Being prepared with the right paperwork the first time prevents the delays that frustrate so many borrowers and business owners.

Here is a breakdown of common banking situations and the documents they typically require:

| Banking situation | Document type | What the bank is verifying |

|---|---|---|

| Mortgage or home loan | Affidavit of identity or occupancy | Your identity and intended property use |

| Business account opening | Corporate resolution or letter of authority | Who is authorized to act for the company |

| Power of attorney banking | Power of attorney document | Legal authority to manage another’s funds |

| Foreign or international accounts | Notarized signature verification forms | Identity and consent for cross-border access |

| Estate or probate matters | Affidavit of executor or administrator | Legal standing to access or close accounts |

| Beneficiary or account changes | Statutory declaration or solemn declaration | Confirmation of intent and identity |

Learning more about affidavits for banks can help you choose the exact document type your lender or institution is asking for. There is a meaningful difference between an affidavit of identity and a statutory declaration, and getting the wrong one notarized can send you back to square one.

Beyond what is listed in the table, these are some common notarized banking documents that clients frequently need:

- Corporate resolutions confirming board authority for financial transactions

- Affidavits of identity when a name discrepancy exists across different documents

- Travel consent letters when guardians need to access accounts on behalf of minors

- International account opening forms required by foreign financial institutions

- Statutory declarations confirming marital status or dependency for benefit-related accounts

When you are dealing with multiple documents, it helps to handle them together. Multiple document notarization in one session can save you considerable time and reduce back-and-forth with your bank.

One often-overlooked operational detail: mortgage approvals can take longer than borrowers expect, and lenders sometimes request updated paperwork close to the funding date. If your notarized document was prepared weeks earlier, it may fall outside the lender’s accepted validity window and need to be redone.

Pro Tip: Before your bank appointment, ask the institution for a written document checklist. Many branches have specific instructions that differ from what is posted online, and a five-minute phone call can prevent an extra trip.

How to get documents notarized for banks in Ontario

Identifying your document is just the start. Here is how to make the notarization process smooth, especially when you are dealing with time-sensitive banking matters, out-of-province situations, or international requirements.

Step 1: Confirm the exact document your bank needs. Call or visit your bank and ask specifically which documents need notarization, which form they should take, and whether a digital or physical copy is acceptable. Get this in writing if possible.

Step 2: Prepare your documents completely before contacting a notary. Notaries review and witness, they do not write your documents for you. Have the correct form ready, filled in accurately, and unsigned. You sign in front of the notary, not before.

Step 3: Gather your government-issued identification. Most notarizations require at least one piece of primary government-issued photo ID and sometimes a secondary piece. Review the online notary steps to understand exactly what is expected before your session.

Step 4: Choose between in-person and online notarization. Ontario now allows remote notarization for most document types. The remote notarization guide explains the full process, including how video-based sessions work for banking documents.

Step 5: Submit notarized documents to your bank. Confirm delivery method. Some banks accept secure digital uploads; others require the original wet-ink notarized document in person.

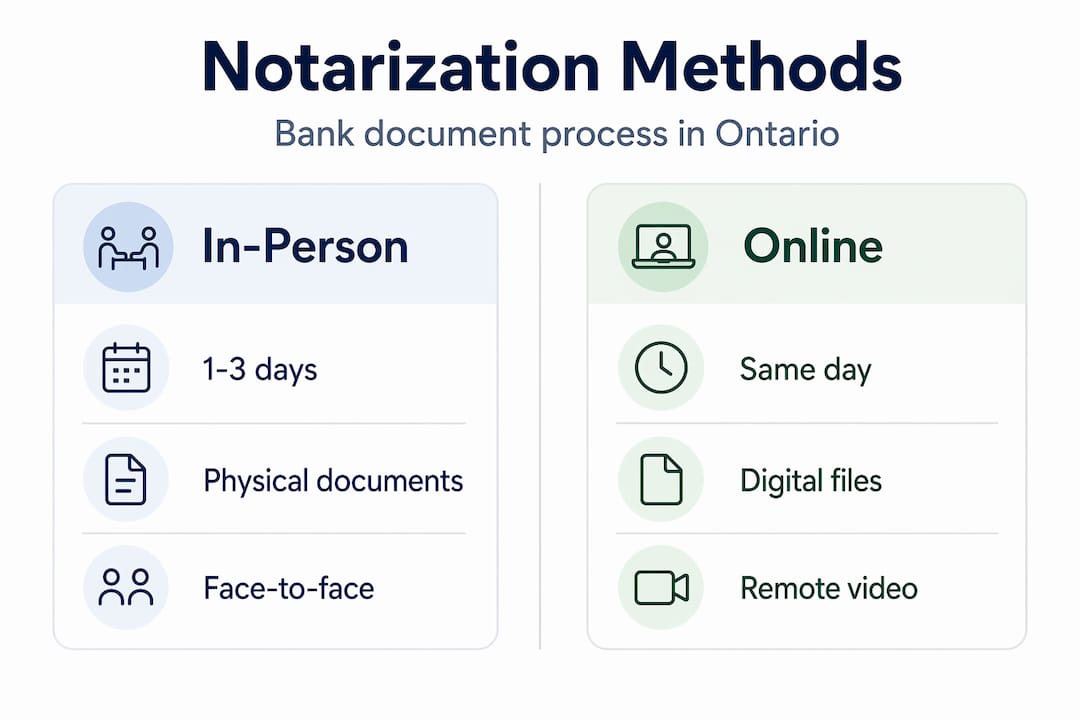

Here is a practical comparison to help you decide which approach works best for your situation:

| Factor | In-person notarization | Online notarization |

|---|---|---|

| Average time to complete | 1 to 3 business days | Same day or next day |

| Typical cost range in Ontario | $50 to $200 per document | $75 to $150 per document |

| Travel required | Yes | No |

| Bank acceptance rate | Universal | Most banks, check first |

| Best for | Complex multi-party documents | Standard affidavits and declarations |

Pro Tip: Always ask your bank whether they accept electronically notarized documents or require an original physical signature with a notarial seal. Some institutions, particularly older or smaller credit unions, may not yet have internal policies in place for electronic notarizations.

One important note if your documents are headed overseas: documents used outside Canada often require additional steps beyond standard notarization. Authentication by Global Affairs Canada, and sometimes an apostille for countries that accept it, may be required before a foreign bank or institution will recognize the document. Consult international authentication guidance to understand what the receiving country requires before you start the process.

Key mistakes and expert tips for notarization success

Now that you understand the process, here is how to make sure you avoid the most common banking notarization pitfalls. These mistakes appear frequently and each one has the potential to delay your loan, account access, or business transaction by days or even weeks.

The most costly mistakes people make:

- Waiting until the last minute. A mortgage closing date is not flexible. If you need a notarized affidavit and you book a notary two days before closing, any issue, including a mismatch in your name or an expired piece of ID, can derail everything.

- Misreading bank instructions. Instructions posted on a bank’s website are often general. The specific branch or department handling your loan may have additional or different requirements. Always confirm directly.

- Bringing the wrong ID to a notarization session. Expired ID, a photocopy, or a secondary document only will not work. Notaries require valid government-issued photo ID in most cases.

- Getting the wrong document type notarized. An affidavit of identity is not the same as a statutory declaration. Your bank asking for one and receiving the other can invalidate the submission entirely.

- Skipping authentication for international use. If the document needs to be recognized by a foreign bank or government, notarization alone is rarely enough. This is a common and expensive oversight.

- Not confirming validity windows. Delays in mortgage approvals often happen when lenders request updated documents close to funding and the existing notarized paperwork has already passed its accepted date range.

Here are the tips that actually prevent these problems:

- Start the notarization process as soon as you receive the lender’s document list, not after you get conditional approval.

- Ask your lender in writing whether there is a validity window on notarized documents. Some require documents dated within 30 days of closing; others accept 90 days.

- Use faster online notarization when you are working against a tight deadline, since same-day appointments are often available.

- Keep a digital copy of every notarized document in a secure cloud folder so you can reference it and resubmit quickly if needed.

- For business banking, ensure that all directors or authorized signatories listed on corporate documents match what is registered with the province.

The real efficiency gain: Online notarization, when done with proper preparation, can cut total processing time by up to 40% compared to scheduling in-person appointments, traveling, and waiting for physical delivery. That matters enormously when you are in the middle of a time-sensitive real estate or business financing transaction.

The practical truth about notarized bank documents in Ontario

Here is the opinion that most official guides will not give you. The biggest source of delay in banking notarization is almost never the notarization itself. The notary appointment usually takes less than thirty minutes. The real problem is the back-and-forth between clients and their banks about what exactly is needed and when.

We see it constantly. A client gets a notarized affidavit prepared within 24 hours, submits it to their lender, and then waits five business days only to hear that the bank needs the document in a slightly different format or that the name on the affidavit does not match the name on the mortgage application. The notarization was fine. The process around it was not managed well.

What banks are genuinely concerned about is not whether you have a fancy notarial stamp on your document. They care about three things: confirming that you are who you say you are, verifying that the request or transaction is legitimate, and ensuring that the paperwork reflects your current circumstances, not your situation from three months ago.

Understanding what notaries really do helps set realistic expectations. A notary confirms your identity and witnesses your signature. They are not vouching for the content of the document or the merits of your loan application. Banks know this. So they layer notarization on top of their own verification processes, not instead of them.

The uncomfortable truth is that rushing notarization without first clarifying requirements almost always leads to more delays, not fewer. The savviest borrowers and business owners we work with treat notarization as one item on a broader checklist, not as a last-minute task. They ask their lenders for written confirmation of requirements, they book notarization sessions early, and they confirm validity windows before closing day arrives. That discipline is what separates smooth closings from stressful ones.

Get help with notarized banking documents in Ontario

Navigating banking notarization requirements in Ontario does not have to be complicated when you have the right support. Whether you are dealing with a mortgage affidavit, a corporate resolution for a business account, or an international banking form that needs to go overseas, having access to a reliable online notary service can make a meaningful difference.

The Online Notary provides fast, secure Ontario online notary services for affidavits, statutory declarations, solemn declarations, invitation letters, and more, all without leaving your home or office. If you are working against a deadline or simply want to avoid the back-and-forth of coordinating an in-person appointment, you can find online notary solutions that work around your schedule, not the other way around. Start your session today and get your banking documents handled the same day.

Frequently asked questions

Do banks in Ontario require all documents to be notarized for loans?

No, only specific documents like affidavits or powers of attorney typically need notarization. Many standard bank forms only require original identification and your original signature.

What is the difference between notarization and authentication for banking documents?

Notarization confirms your identity and witnesses your signature on a document. Authentication or apostille is an additional step required when a document must be recognized by a foreign government or financial institution outside Canada.

How long are notarized documents valid for bank transactions?

Most banks require notarized documents dated within 30 to 90 days of the transaction. Confirm the exact window with your lender in advance, because validity windows vary between institutions and can catch borrowers off guard near closing.

Can I use online notarization for my documents at Ontario banks?

Many Ontario banks now accept online notarization, but acceptance policies vary by institution and document type. Check directly with your bank’s mortgage or commercial banking department before booking an online session.

What type of ID do I need for notarization at a bank?

You typically need a valid government-issued photo ID as your primary piece, and sometimes a secondary document as well. Original documents are required since photocopies or expired ID will not be accepted during notarization.